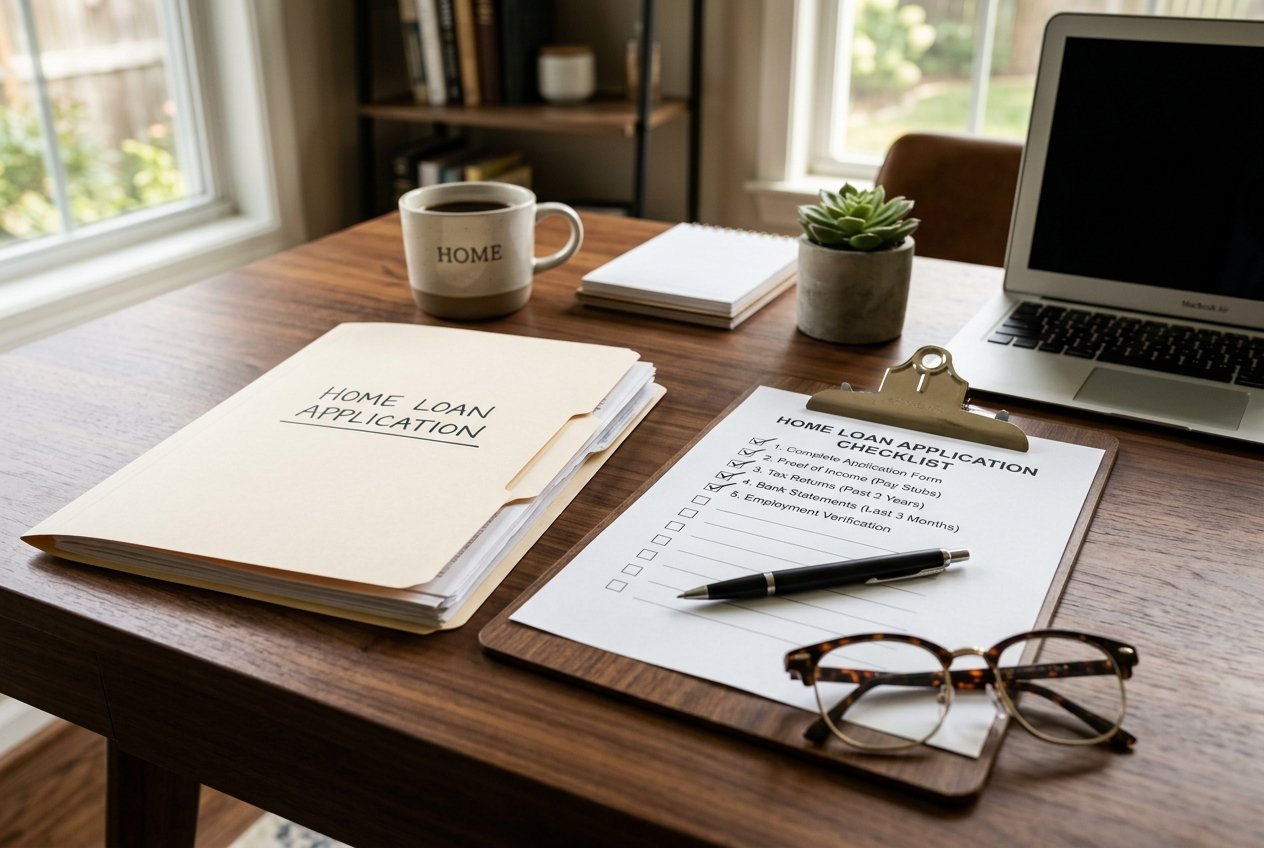

Applying for a home loan in India involves a meticulous underwriting process where banks evaluate your financial stability, legal property titles, and repayment capabilities. While calculations and rate comparisons are exciting steps, documentation is where most applications succeed or stall. Submitting incomplete, outdated, or unverified documents can lead to lengthy clarification cycles or outright rejection. Having a pre-compiled dossier ready accelerates the approval window, turning a potential multi-week headache into a seamless process.

The Baseline: KYC & Identification Paperwork

Every applicant and co-applicant must provide clear, verified KYC (Know Your Customer) papers. These are mandatory legal identity checks required by all financial institutions in India:

- PAN Card: Mandatory for tax reporting and credit bureau verification.

- Aadhaar Card: Essential for address validation and e-signing.

- Alternative Address Proofs: If your current residence differs from your Aadhaar address (e.g., utility bill, rent agreement, passport).

- Passport Size Photographs: Typically 3 copies of all applicants.

Document Checklist for Salaried Professionals

Lenders view salaried individuals as having steady cash flows. To verify your income consistency, prepare the following paperwork:

| Salaried Document | Period/Format Required |

|---|---|

| Salary Slips | Latest 3 to 6 Months (Clearly showing tax deductions, PF, and net pay) |

| Bank Statements | Latest 6 Months (Salary account statement showing monthly credit entry) |

| Form 16 & ITR | Latest 2 Assessment Years |

| Employment Certificate | Official letter detailing designation, joining date, and active status |

Document Checklist for Self-Employed Individuals

Lenders inspect self-employed applications closely to gauge business viability and net annual profits. Prepare these business files:

- ITR (Income Tax Returns): Detailed filing receipts for the last 3 assessment years, showing computations.

- Audited Financial Statements: Certified balance sheet and profit & loss statements for the last 3 years, audited by a CA.

- Business Bank Statements: Latest 12 months' statements for all current accounts of the business.

- Business Existence Proof: GST registration, Partnership deed, MOA, shop & establishment certificate, or tax registration certificates.

- Professional Degree: (Required for doctors, CAs, architects, etc.)

Essential Property Paperwork

Even if your personal income is stellar, a home loan is ultimately a secured mortgage. The lender's legal department must audit the property's titles to ensure it is free from disputes. You must submit:

- Allotment Letter / Builder-Buyer Agreement: From the developer in case of fresh construction.

- Original Sale Deed: Tracing the ownership history (Chain of ownership docs in case of resale property).

- Approved Building Plan: Approved layout copy from local municipal authorities.

- NOC (No Objection Certificate): From the housing society or developer.

- Encumbrance Certificate: Proving the property has no existing bank liens or legal disputes.

Doorstep Document Guidance by Easy Home Loan DSA

Collatng all these legal files can feel overwhelming. "That's why we offer end-to-end doorstep document services," says Sahiba Kheterpal. "We visit your home or office, organize your files into a clean digital packet, pre-check them for anomalies, and submit them directly to bank underwriters. You don't have to visit bank branches or handle photocopies yourself."

Pooja Sabharwal emphasizes: "We ensure your Form 16 details align perfectly with your bank statement salary credits. If there is a variation due to bonuses or deductions, we explain it to the credit manager upfront to prevent processing delays."

Ready with Your Documents? Let Us Pre-Check Them

Avoid delays. Connect with Pooja or Sahiba to schedule a free doorstep document collection and verification check today.

Schedule Doorstep Consultation